Date: Saturday, 25 July 2020

A financial, geoeconomic and geopolitical analysis

Saturday July 25, 2020

In this article, the author (1) offers us a documented analysis of Djibouti's debt and over-indebtedness, in connection with the construction of the section of the railway line for Ethiopia. It is not only a financial subject but a geoeconomic and geopolitical approach. The link is made between, on the one hand, a low profitability of the completed project (random supply of electricity, lack of products to export, cyclical deterioration) and of course the issues of influence (rights of use of the naval base, creation of 'a political clientele of countries, technological showcase for China ...), without excluding management errors ... Africa remains a field of experimentation for China ("split-diplomacy", diplomacy of the "big gap ») And emerging countries. The reading of the debt is not unequivocal: it stems from the complexity of the issues and the relations between a strong economy and a country in difficulty. This is the meaning of the author's thesis: over-indebtedness does not necessarily translate a calculation but results from an enormous imbalance of power.

DJIBOUTI'S CHINESE DEBT. TP

1. OPENING

On July 15, 2019, Ilyas Moussa Dawaleh, Minister of Economy and Finance of Djibouti, "tweeted" on Twitter to announce that the restructuring of the loan from the ExIm Bank of China for the construction of the Djiboutian section of the Djibouti - Addis Ababa railway would be acquired even if "a few small details" remained to be resolved. He returned to Beijing a month later, on August 7, to discuss these details; the atmosphere no longer seems to be at the party despite "the quality of the exchanges" mentioned by the minister, if we judge by the two photos he posts on Twitter where the three Djiboutian envoys (including him) have to face ten representatives of the ExIm Bank of China.

Published on October 23, 2019, an IMF report is a little more explicit about the situation, but its interpretation is not obvious, especially as it suggests that the renegotiation would not have been finalized. The railway project between Ethiopia and Djibouti is a project of some four billion dollars that Djibouti had to finance to the tune of 550 million dollars for the part built on its territory, both from its own funds (58 million dollars) than by a commercial loan of 492 million dollars granted in 2013 by the ExIm Bank of China. If the work is well finished, on the other hand the operation of the line has proved disappointing for the time being, both for the lack of a random supply of electricity and a deficit of products to be exported.

According to Ilyas Moussa Dawaleh and the IMF, this renegotiation would have made it possible to lengthen the term of the loan from fifteen to thirty years and the length of the deferred payment which would go from five to ten years. As for the interest rate, its modulation is less obvious, because it is the sum of two elements. The first element is a known fixed rate (spread) which serves to guarantee a minimum return to the lender and to cover its administrative costs. The second element is not immediately quantified, but it must be equal to the interbank interest rate practiced on the London financial market (LIBOR or London Inter-bank Offered Rate). In this case, the benchmark LIBOR rate is that of the US dollar for loans with a maturity of six months. If these last two details (currency and maturity) express a choice among five different currencies and seven different maturities, it hardly allows to know the exact amount of the interest rate which will actually apply los a given maturity. We can only see that the interest rate on the loan of the ExIm Bank of China would have been reduced from LIBOR plus 3.0% to LIBOR plus 2.1%. However, the six-month LIBOR has historically been able - on an annual average - to reach 8.133% in 1988 and 0.329% in 2014. In other words, small increments or spreads do not mean low interest rates. Sri Lanka has paid the price. For phase 1 of the construction of the port of Hambantota, in 2007, Sri Lanka borrowed 307 million dollars from the ExIm Bank of China at the fixed rate of 6.3% (to which would have been added a spread of 0, 75%) in preference to a rate calculated on LIBOR, as the latter having experienced a period of continuous rise since 2003, the Sri Lankan authorities preferred the certainty of a fixed rate; the choice was unfortunate since the price of LIBOR was reversed in 2008 before stabilizing quite low from 2010. Indirectly, we can see how high the ExIm Bank of China would estimate the fair amount of its remuneration.

Obviously, a variable rate does not facilitate budgetary planning of disbursements (principal repayments and interest payments). It also accentuates the difficulties in appreciating the weight of debt and the cost of renegotiation, so we are going to review what started the crisis.

2. AMORTIZATION OF A LOAN

At the beginning of our history, there is the question of the amortization of a loan, of several loans should we say. At the same time as a loan to finance the railway project, Djibouti obtained from the ExIm Bank of China, a second commercial loan in the amount of 322 million dollars with the same conditions of duration and interest rate. , for a drinking water supply project between Ethiopia and Djibouti. We must also add a loan of 580 million dollars granted in 2013, again by the ExIm Bank of China, for port developments: on the one hand for the multipurpose port of Doraleh (340 million dollars) and on the other hand for the Damerjog cattle port ($ 240 million). To our knowledge, these latter loans have not been renegotiated. Other loans, much smaller in size, were also contracted,

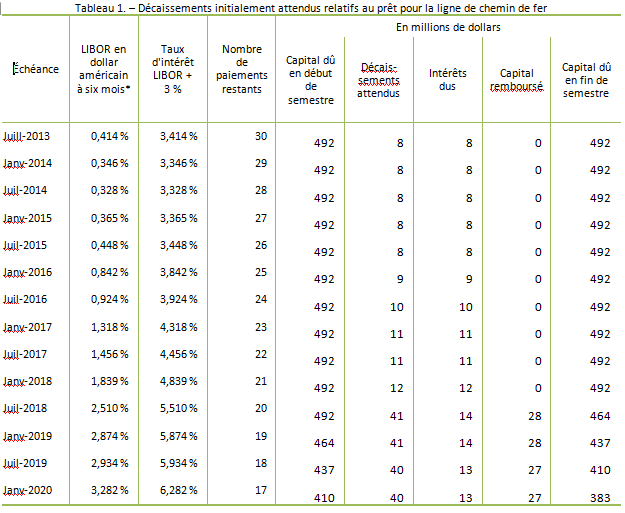

Given the variations in LIBOR and deferred payments, we can attempt to estimate the amount of disbursements that the government of Djibouti should have faced from 2019. Remember that a deferred payment is not an exemption from the payment of accrued interest, this is added to the principal if it is not paid during the year concerned - the sum of the principal and the interest serving as the basis for calculating the interest for the following period. In the cases which concern us, the interest for one year was paid in the year it was due, only the repayment of the principal being carried over from one year to the next until the expiry of the deferred payment. In Table 1,we give the calculations for the amortization of the loan for the Djibouti - Addis Ababa railway line. This reconstitution is very likely accurate insofar as the amount of capital remaining due at the end of 2018 is comparable to the figure put forward by the World Bank in its September 2019 report on Djibouti's debt vulnerability. However, in terms of details, there may be slight differences - if only because of the rounding. Anyway, during the second half of 2018, the expected disbursement amount would have been $ 41.2 million (compared to $ 11.9 million the previous half).

Sources: Author's calculations from Global-Rates.com

At the same time, however, the economic situation seemed to be reversed, all the more so as the railway line was not operational and doubts were emerging as to its profitability (see below). Not only are the expected revenues not there, but Djibouti is also suffering from a deterioration of the financial environment. From July 2013 to January 2019, the benchmark LIBOR having continuously increased, the interest rate paid rose from 3.506% to 5.874%, i.e. a 2.5-fold increase in the semi-annual cost of the loan. As interest was regularly paid, no arrears were added to the principal owed to the ExIm Bank until the end of 2018. Unfortunately, at the start of 2019, what the evolution of the money market suggests is a continued increase in LIBOR, ipso facto making debt service even heavier. Let us add that the real exchange rate of the Djiboutian franc having deteriorated compared to the nominal exchange rate, the profit which Djibouti could have derived from it by collecting additional dollars against rising exports, is considerably limited given the very weak exporting capacities of the country. The will to develop is turning into a veritable infernal debt machine, because at the very moment when Djibouti must amortize this loan, the other two loans mentioned above must begin to be amortized too.

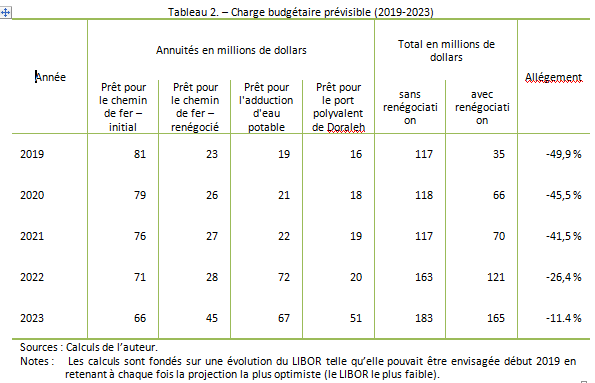

When Djiboutian leaders become aware of the situation and decide to renegotiate their debt, the situation they can foresee is undoubtedly the one we describe in Table 2based on fragmentary data that the IMF and the World Bank provide us with a dropper and taking into account a development of LIBOR as it could be envisaged at the beginning of 2019. First, the loan for the Djibouti section of the line Djibouti - Addis Ababa would have required the payment of $ 81 million for the year 2019; to this figure, should be added the annuities corresponding to the interest on loans for the drinking water supply and the port of Doraleh (respectively 19 and 16 million dollars according to these calculations), that is to say in all 117 million dollars. And so on in subsequent years as long as the grace periods for the other two loans were not exhausted. If we relate this charge to the programmed amount of the 2019 and 2020 budgets, it would therefore be a charge corresponding to around 14% of the respective budgets. In terms of GDP, this burden would represent respectively more than 4% of the national wealth that would be created over the same two years. Whatever the inaccuracies of our calculations, we understand the concern of the leaders and their urgency to want to renegotiate at least part of these loans.

The choice fell on the loan granted for the construction of the railway line, not only because of its weight, but also probably because the Djiboutian government knew that the Ethiopian government had undertaken to renegotiate the restructuring of the railway. loan he had taken out to finance this joint railway project. By extending the payment deferral from 5 to 10 years, this would result in an additional grace period of five years; In the immediate future, the Djibouti government can therefore hope for a reduction in its burden of nearly 50% the first year and more than 40% the following two years.

3. THE COST AND PROFITABILITY OF A RENEGOCIATION

In fact, the evolution of LIBOR peaked in early 2019 and then fell and suggests a subsequent calmer period which, most certainly, positively influenced the projections of the IMF and the World Bank. However, the available data cannot always be easily aggregated to obtain a clear and perfectly understandable view of the situation both of the debtor - in this case, Djibouti - and that of its creditors. In their 2019 report entitled Djibouti: 2019 Consultations under Article IV, the two institutions take stock of Djibouti's external debt; it shows that, at the end of 2018, 53.3% of Djibouti's external debt consisted of Chinese debts and that their total weight was equivalent to 40.

Djibouti's debt is essentially a debt owed to public creditors, with China's share having increased considerably in recent years and deferred payments coming due, the burden of the related debt service has increased considerably between 2019 and 2021, rising from $ 48 million in 2019 to $ 82 million the following year (+ 71% year-on-year) then to $ 104 million in 2021, an increase of 120% in two years, or nearly two-thirds of Djibouti's external debt service (60.7%). China is also the bilateral creditor whose service is by far the most important since on average over the three years 2019-2020-2021, it will receive 80% of this service. In short,

It is impossible for us to predict the evolution of LIBOR, starting from an estimate of the cost of a loan and the additional cost due to its restructuring. However, we can make assumptions and engage in simulations. It appears that the immediate consequences of a restructuring are to avoid the peak of disbursements of 2019 and to delay the most important of them which will never be as high as what the initial contract could cause. The other consequence is obviously the lengthening of the process. It is also clear that variations in LIBOR have little impact on the value of the process (relief of disbursements) even if it results in an increase in the cost of the loan. In the case of our simulations, the additional cost resulting from the negotiation could increase from 24% to 39% of the amount of the initial loan (492 million dollars).

4. PROFITABILITY, FEASIBILITY AND RELEVANCE

For China considered as a whole, the profitability of the loan of its ExIm Bank is not only financial, but also economic. The granting of this loan is linked to the recourse by the Djiboutian authorities - and Ethiopians on their own territory - to Chinese companies, both to companies providing services which carry out public works operations, but also to companies which produce rolling stock (locomotives and wagons), rails, signage and all other elements necessary for the construction of the work. In other words, even if the financial profitability of the project was zero or only low, the project would generate in a Keynesian way profit and growth in Chinese territory. When the World Bank or structures like AFD finance projects - but this is undoubtedly also the case for most of the Paris Club members - they cannot compensate for the low rate of return by sponsoring their own companies. . In addition, still for these structures, the loaned capital being very mainly spent in the borrowing country, they come to stimulate its economic activity, unlike Chinese companies which import everything from China, including the food of their workers who are also often imported. .

The reduction in disbursements resulting from the renegotiation is certainly welcome for Djibouti's budget. However, it would have been much more advisable on the part of the Chinese advisers and the ExIm Bank of China to have initially ensured the profitability of the project they had designed (or even its real feasibility) before financing it. and above all not to have powerfully encouraged Djibouti (but also Ethiopia beforehand) to choose a solution, certainly splendid (a real showcase for Chinese technologies), but absurdly expensive for very poor countries and in terms of profitability currently more limited and more uncertain in the longer term.

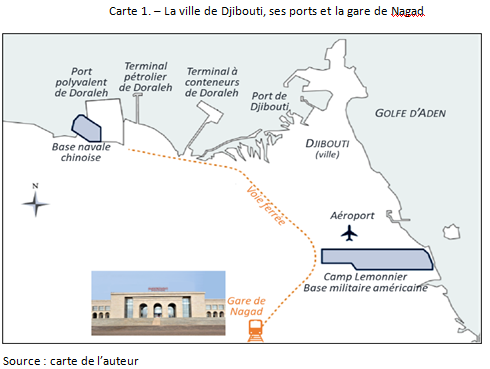

The renegotiation would also have had indirect costs - not to say hidden - which are more difficult to prove. The first of these costs would have been to vote in favor of the Chinese candidate, Qu Dongyu, as director of the FAO. We know that China's interest (China, not Chinese companies) in Africa is far more political than economic. Note that the vote took place on June 23, 2019, that is to say shortly before the first visit - this one apparently happy - of Ilyas Moussa Dawaleh to the ExIm Bank in Beijing. The second price to pay would be the granting of works to extend and develop the Djibouti - Addis Ababa railway line from the Nagad terminal station (twelve kilometers from the city of Djibouti in the middle of nowhere) to the port terminals and beyond to the Chinese naval base. This work would be entrusted to a Chinese company and would be the subject of an additional loan from the ExIm Bank. What is implausible in this story - which indirectly could prove it - is that we wonder why it was necessary to wait for this Djiboutian budget crisis to decide to undertake this essential work. This is essential for the smooth operation and profitability of the line, since Ethiopian containers intended for export must be transported to port terminals, whether it is the container terminal in Doraleh or the multipurpose terminal in Doraleh. In any event, we can conclude that the ExIm Bank initially granted a loan without carrying out any real feasibility and profitability studies which should have been imposed on it to protect its funds. The third price to pay,

5. DEBT DIPLOMACY?

"There are two ways of conquering and enslaving a nation, one is by arms, the other by debt," said John Adams (1735-1826), second president of the United States. We have already suggested that China may seek to build up a political clientele through its loans. In saying this, we imagined that she was only asking for the recognition that would be due to a brother country allied in the spirit of Bandung to obtain the support of African countries and other developing countries along the new Silk Roads. . In the interview that the president of the ExIm Bank of China, Zhang Qingsong, gives to the Chinese national public broadcaster CCTV on April 23, 2020, he claims that 1,800 projects along the new silk roads would benefit from financial assistance from his bank, which would have contributed a trillion renminbi - nearly $ 150 billion. Zhang Qingsong also emphasizes the role of these financial relations, of these sovereign loans and borrowings to emphasize that they serve the internationalization of the renminbi. In this sense, it is clearly an assumed policy of influence and not a simple extension of a commercial strategy. However, and despite the enormity of the figures cited, I do not imagine that they could manifest a conspiracy hatched in the secrecy of the Zhongnanghai kitchens in order to induce countries in debt beyond their repayment capacity,

To tell the truth, Sri Lankan over-indebtedness was most certainly the result of ex-President Mahinda Rajapaksa's desire to be re-elected whatever the price his country would pay as well as a certain Chinese pusillanimity - corrupting per se, starting with a certain fear of change - only of Beijing's conscious and thoughtful debt strategy. Be that as it may, it is a company - precisely the China Merchants Port which operates in Djibouti - which bought back the Sri Lankan debt so that the new Sri Lankan government could reimburse "China" - or more exactly to the Sri Lankan government. Chinese lending financial institution (ExIm Bank of China) - its debts ($ 1.2 billion) relating to the port of Hambantota. In exchange, the company (i.e. CMPort and not China) has obtained a 99-year concession which should allow it both to repay the bouquet of $ 1.2 billion and to build and then operate infrastructure ports, whose property is ultimately and remains that of Sri Lanka. Isn't this, moreover, one of the lessons given by the handover of Hong Kong?

What we have to see again is that the individual strategies of a series of Chinese actors (CCCC, CHEC, CMPort, ExIm Bank and others) have met in Sri Lanka - as in Djibouti and elsewhere - and are added together, but they do not represent or express a strategy of the Chinese government with regard to Hambantota, Sri Lanka or Djibouti. There is therefore an essentialization of China which undoubtedly can only obstruct our understanding of Chinese presences in the world; hence the discourse is lost in an inopportune and sterile China bashing and turns away from a legitimate and justified criticism of all the actors - Chinese or not; governmental or not - as suggested in paragraph 47 of the Report of the International Conference on Financing for Development,

Sustainable debt financing is an important element in mobilizing resources for public and private investment. Comprehensive national strategies to monitor and manage external liabilities, within the framework of national debt sustainability conditions, including sound macroeconomic policies and sound management of public resources, are an essential element in reducing national vulnerabilities. Creditors and debtors must be equally responsible [emphasis added] for preventing and resolving an unsustainable debt situation.

Thierry Pairault, July 23, 2020

A summary table on the main financing projects (total cost, state of progress, financing)